Amortization Calculator

| Enter Loan Data |

|---|

| Loan Amount | |

| Annual Interest Rate | |

| Loan Duration | |

| Start Date | |

| Extra Payments |

The loan will be paid off in 120 month(s) without extra payments. |

| Total of 120 Payments | $260,463.07 |

| Monthly Payment | $2,170.53 |

| Total Interest | $60,463.07 |

| Loan Distribution |

|---|

| Loan Balance, Interest Payments |

|---|

Monthly amortization schedule ↑

| Year | Opening balance | Interest | Principal | Ending balance |

|---|---|---|---|---|

| Year 1 | $200,000.00 | $10,614.85 | $15,431.45 | $184,568.55 |

| Year 2 | $184,568.55 | $9,744.40 | $16,301.91 | $168,266.64 |

| Year 3 | $168,266.64 | $8,824.84 | $17,221.47 | $151,045.17 |

| Year 4 | $151,045.17 | $7,853.42 | $18,192.89 | $132,852.28 |

| Year 5 | $132,852.28 | $6,827.19 | $19,219.11 | $113,633.17 |

| Year 6 | $113,633.17 | $5,743.08 | $20,303.22 | $93,329.95 |

| Year 7 | $93,329.95 | $4,597.82 | $21,448.48 | $71,881.46 |

| Year 8 | $71,881.46 | $3,387.96 | $22,658.35 | $49,223.12 |

| Year 9 | $49,223.12 | $2,109.85 | $23,936.46 | $25,286.66 |

| Year 10 | $25,286.66 | $759.65 | $25,286.66 | $0.00 |

What to Know About Amortization?

In accounting, amortization refers to the systematic expensing of an intangible asset’s cost (e.g., patents or goodwill) over its useful life. This reduces the asset’s book value on the balance sheet while recording periodic expenses on the income statement, reflecting its declining utility.

In finance, amortization is the process of paying off a debt, such as a mortgage, car loan, or personal loan, over time through a series of regular payments. These payments reduce the loan balance—a liability on the balance sheet—until it’s fully paid off. Amortization is available in the more specific calculators, like loan calculator or car loan calculator. Further here, we’ll cover especially financial amortization.

How Does Amortization Work?

To understand amortization fully, it’s helpful to explore how each payment is calculated and applied. This is best illustrated through an amortization schedule, a table that details every payment over the life of the loan.

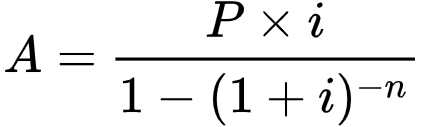

Equal installment (A) for an amortized loan is determined using the annuity-immediate formula:

Where:

A = Total payment every period;

i = Periodic interest rate;

P = Present value, or the initial loan amount (principal);

n = Total number of installments.

Once the periodic payment (A) is known, the amortization schedule is built by calculating the interest and principal portions for each period:

- Interest Payment: Multiply the remaining loan balance by the monthly interest rate (i).

Example: If the balance is $200,000 and the monthly rate is 0.3333% (4% annual rate ÷ 12), the interest is $200,000 × 0.003333 = $666.67. - Principal Payment: Take away the interest payment from the total monthly payment (A).

Example: If A is $954.83, the principal payment is $954.83 - $666.67 = $288.16. - Remaining Balance: Take away the principal payment from the previous balance.

Example: $200,000 - $288.16 = $199,711.84.

This process repeats each period, with the interest payment decreasing (due to a lower balance) and the principal payment increasing, while the total payment stays constant.

Example Amortization Schedule

Consider a $200,000 mortgage with a 4% annual interest rate and a 30-year term (360 monthly payments). Using the annuity formula above, the monthly payment is approximately $954.83. Here’s how the first two payments might look:

| Date | Periodic Payment | Interest Payment | Principal Payment | Remaining Balance |

|---|---|---|---|---|

| 05/2024 | $954.83 | $666.67 | $288.16 | $199,711.84 |

| 06/2024 | $954.83 | $665.71 | $289.12 | $199,422.72 |

Over time, the interest portion shrinks, and the principal portion grows, accelerating the reduction of the balance until it reaches zero after 360 payments.